1999 is back, and I’ve missed it. Ever since then, I’ve been chasing that next 50-bagger, the kind of life-changing winner that helped me come up with the down payment for my first property. But he’s been elusive.

I still remember sitting on the international trading floor at Goldman Sachs at 1 New York Plaza, glued to my screen as internet names like Commerce One and Yahoo soared higher almost daily. My firm had just gone public, instantly turning the partners into decamillionaires. The energy was electric – optimism everywhere, fortunes being made, CNBC blaring nonstop.

Fast forward to today: tech stocks are leading again, crypto investors are buying Lambos, and AI is woven into everything – our phones, portfolios, and daily conversations. San Francisco, once quiet during the pandemic, is buzzing again. Startups are hiring and everyone’s talking about the next big thing.

And I’ll admit, I’m hyped.

Then the 2000 dot-com crash vaporized trillions in wealth and taught me one of the most important lessons of my life: euphoria always feels rational until it doesn’t. Ah, cheers to irrational exuberance.

The Return Of The 1999 Atmosphere

I’m investing in public tech stocks, private growth stocks, a little bit of Bitcoin, and San Francisco real estate, which all feel poised for continued growth.

Back in 1999, I promised myself that if the mania ever returned, I’d lean in harder, but smarter. Now, with investors once again betting on infinite growth, that time has come.

So how do we balance greed with wisdom? How do we ride this wave of innovation without repeating the mistakes of the past? Let’s explore what history teaches us and how to navigate this AI-driven rocket responsibly.

Because frankly, with far more capital at stake, I don’t want to lose my shirt again. But even if I do, I’ve heard the “dad bod” is the most attractive male body type, making us feel approachable, stable, and mature.

What Makes This Time Different (and What Doesn’t)

Yes, this time is different, and that’s exactly what everyone says before every bubble bursts. But there are some key distinctions worth acknowledging.

- AI has tangible productivity effects. Unlike many dot-com ideas that never made money, AI is already saving companies billions.

- Balance sheets are stronger. Corporate debt loads are healthier than in 1999 and 2007, and many firms are flush with cash.

- Strong income and cash flow. In addition, the largest tech companies are generating enormous free cash flow.

- Monetary policy is turning supportive again. Amazingly, the Fed is resuming its interest rate cuts with everything at all-time highs, providing a tailwind for risk assets.

That said, the psychology of manias never changes. People overestimate short-term gains and underestimate long-term disruption. AI is real, but that doesn’t mean every AI stock is. Some companies will go to the moon; the vast majority will go to zero.

That’s why perspective and diversification matter more than ever.

How I’m Positioning for The New Mania

Here’s how I’m approaching this cycle, and some suggestions if you’re feeling swept up by the hype. As we should all remember, there are no guarantees in risk assets. Always do your due diligence and invest according to your own goals and risk tolerance.

1. Stay Invested, But Maintain Exposure Limits

I’m fully participating in this bull run but will trim individual positions once they exceed 10% of my portfolio. A concentrated portfolio works, until it doesn’t.

The 10% threshold is somewhat arbitrary. You should come up with your own comfort level. According to modern portfolio theory and supporting studies, holding around 20 to 30 positions is typically enough to achieve most of the benefits of diversification along the efficient frontier, roughly a 3% to 5% allocation per position.

It’s not enough to just monitor your investment portfolio’s composition, you also need to view it in the context of your overall net worth. Look at how much you have in cash, real estate, alternatives, bonds, and low-risk assets.

Personally, I aim to keep public equities between 25% and 35% of my total net worth. That allocation gives me the confidence to stay the course during downturns. If the average bear market declines about 35%, that would translate to roughly a 10% hit to my overall net worth, which I can comfortably stomach.

Ascertain how much of your net worth you’re comfortable losing.

2. Shift More Towards Real Assets

1999 through 2009 taught me that stocks are funny money with no real utility. You can’t drink your stocks, live in your stocks, or physically enjoy them. The only way to benefit is to sell some shares from time to time to fund a better life.

The best asset I’ve found that offers both potential appreciation and real-world utility is real estate. There’s no better feeling than watching your home appreciate in value while you actually enjoy living in it. If you have children, that satisfaction multiplies. You’re not just building wealth, you’re providing stability and memories for your most precious assets.

I’m long as much San Francisco real estate as I can comfortably handle, a primary residence and three rentals. AI companies are expanding, housing demand is rebounding, and real estate remains one of the few tangible hedges against both tech volatility and inflation.

3. Increasing Private Company Exposure

I’m investing directly into AI companies through various closed and open-ended venture capital funds with up to 20% of my investable capital. All of the closed-end venture capital funds charge 2% and 20% of profits or more, and are invite only. While Fundrise Venture is open to everyone and doesn’t charge any cary.

Back in 1999, I had ~$8,000 to invest after receiving my signing bonus. So I invested $3,000 in VCSY, a Chinese internet company that 50Xed. However, to make life-changing money requires a much larger amount of invested capital. So this time I’m around, I’m investing seven figures while staying within my 20% exposure limit.

Below is a chart that should both scare and excite you. Every venture capital general partner thinks they’ve invested, or will invest, in the next AI winner. But as a 20-year limited partner in venture capital, I’ve seen that roughly 90% of investments either go to zero or return only modest capital.

For that reason, a general partner must either have a tremendous track record or the fund must already own companies you strongly believe in before it’s worth investing. I’m hedged by investing in both types of venture capital funds.

4. Maintain Liquidity To Buy The Dip And Survive

After the 1999–2000 and 2008–2009 downturns, I promised myself I’d always keep at least one year of living expenses in cash or cash equivalents like Treasury bills, and I still do. Liquidity buys peace of mind. It lets you both survive and buy the dip when markets crash.

Thankfully, cash and Treasury bills now pay a handsome ~4% risk-free return. That makes the so-called “cash drag” in a 1999-style bull market far less heavy.

Corrections are inevitable. If you don’t have liquidity ready, you’ll be forced to sit on your hands instead of take full advantage.

5. Do Not Buy Risk Assets On Margin

Although the temptation to leverage up in a 1999-style bull market is high, don’t do it. If we really are reliving 1999, remember what came next: the NASDAQ crashed 39% in 2000 and ultimately fell 78% from peak to trough by 2002. Even if you were only 35% on margin back then, chances are you were wiped out.

Today, plenty of investors are making the same mistake in cryptocurrencies – leveraging 2X to 50X in pursuit of quick riches. Some have made fortunes, but many have also lost years of hard-earned gains in a single day. That most recent day was October 10, 2025, when widespread liquidations erased entire portfolios due to leverage.

If you absolutely can’t resist the urge, limit your speculative capital. Carve out no more than 10% of your investable assets for leveraged punts. And go in knowing the worst-case scenario: not only can you lose everything, you might also owe money to your broker.

In a flash crash, prices can gap down before your broker executes a stop limit sale, leaving you with a negative balance. Investing on margin long-term is a bad idea. Resist the temptation.

6. Embrace The Dumbbell Investing Strategy

During manias, investing FOMO often pushes investors to take excessive risk. You buy things you don’t fully understand simply because you can’t stand watching others get rich without you. More often than not, this type of investing leads to ruin.

One way to manage this is with a dumbbell strategy: split your portfolio or new investments between low-risk or risk-free assets and high-risk, speculative bets. This approach lets you capture upside if the mania continues, while still protecting your downside if it fizzles out.

Over the past several years, I’ve been regularly using the dumbbell strategy to invest in both private AI companies and in Treasury bills and bonds. This way, no matter what happens, I’m hedged.

7. Spend And Enjoy A Portion Of Your Profits

Every year during a bull market, I try to buy something tangible with my “funny money” profits. This ensures that if, and when, the bear market returns, at least I’ll have something to show for the gains.

For example, in 2003, I used profits from VCSY in 2000 to buy a two-bedroom condo with a park view in Pacific Heights, a property I still own today. It housed my girlfriend and me for two years and now generates semi-passive income to help fund our retirement.

You don’t have to invest your funny money in real estate. Fine art, rare books, ancient coins, or even memorable experiences like a family vacation or a cruise for your parents all count. Great experiences often appreciate in value in ways that money can’t measure, especially now that we can record them in stunning 4K.

As long as you continue taking profits to acquire meaningful experiences or material things you value, a 1999-style bull market can keep rewarding you long after it’s technically over.

7. Mentally Prepare For Financial Pain & Mental Anguish

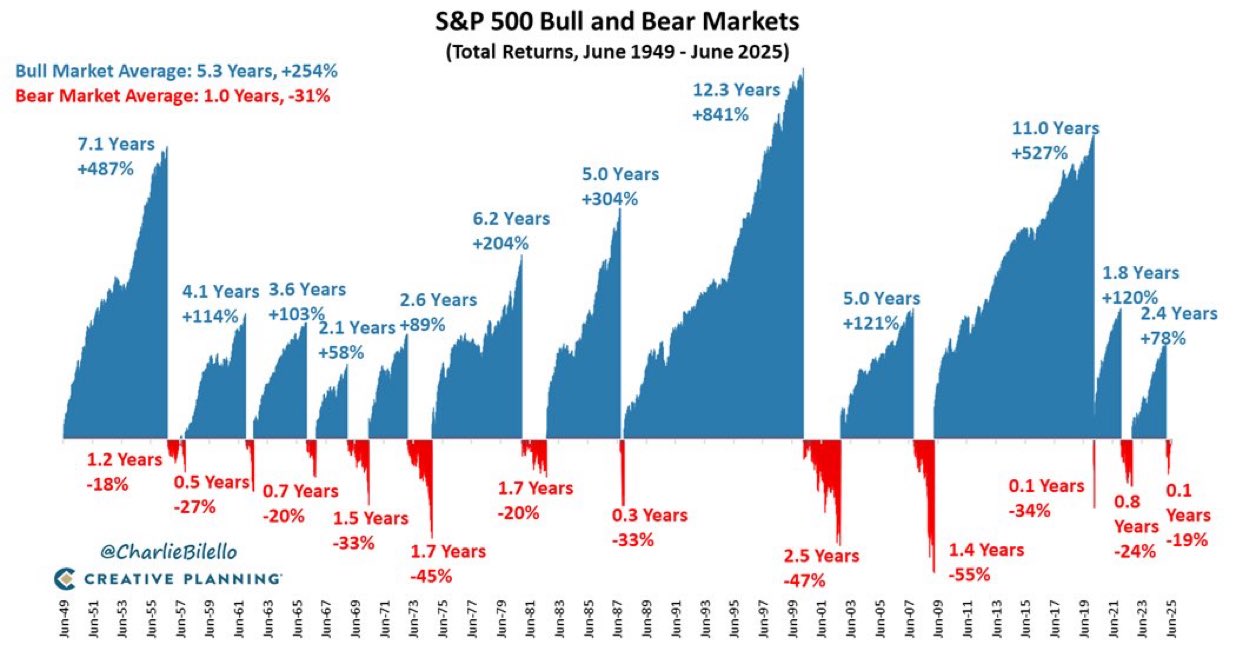

A 1999-style bull market will eventually end badly. We could even face another lost decade, where risk assets provide little to no real returns. It could certainly happen again, especially with the S&P 500 trading at 23X forward earnings.

However, once you study history and understand how severe losses can get, the pain isn’t as shocking when they arrive. Here are some key statistics:

- 5% corrections: happen 3–4 times per year on average.

- 10% corrections: happen about once per year.

- Bear markets (-20%+ declines): from 1928–2025, there have been ~16, averaging one roughly every 5–6 years.

- Average bear market drawdown: ~35%.

- Median post-1946 bear market duration: 11 months, with an average decline of 33–35%.

- Median recovery time to all-time highs: 23 months.

In other words, mentally take your equity exposure and lop off 35% of its value immediately. Ask yourself: can you handle losing that much and waiting roughly two years to get back to even? If yes, you’re good to go. If not, you need to make adjustments.

You can even use my FS-SEER formula to quantify your risk tolerance in terms of time, helping you plan your allocations more confidently.

7. Revisit your income streams.

Your income streams are crucial for staying afloat during a bear market, yet they often get overlooked in a bull market. That’s why it’s important to list out your various sources of income and rank them by reliability. When the bear market hits, how secure will they be?

If you know you’ll always earn enough to cover your family’s living expenses, you can afford to take more risk. But if many of your income streams are likely to collapse in a downturn, you need to adjust your exposure accordingly.

The key is to build diverse sources of income before you actually need them. By the time you do, it may already be too late.

8. Focus On Health And Lifestyle

Bull markets can make you forget what really matters.

Back in 2009, my stress levels were through the roof as I watched roughly 40% of my net worth vanish in six months that took a decade to build. My back pain made it almost impossible to drive or sit, and I was grinding my teeth relentlessly. My TMJ was so bad I couldn’t talk comfortably for more than five minutes at a time. I had to find a way out.

Today, I strive for balance, a goal made far easier without a 60-hour-a-week job. I start the day with 1-2 hours of writing, then often play tennis, coach my kids, and remind myself that wealth is meaningless if you don’t have the energy to enjoy it.

In your pursuit of riches, please do not neglect your health! It will come to bite you in the arse eventually.

Don’t Confuse Brains With a Bull Market

It’s intoxicating to feel smart in a rising market. Gains reinforce confidence, and confidence feeds risk-taking. But the truth is, in bull markets everyone looks brilliant, until the rocket blows up.

When the 2000 crash hit, I I watched colleagues lose everything they’d built over a decade. Markets giveth, and markets taketh away.

Don’t let a bull market convince you that you’re invincible. Let it remind you that discipline is what keeps you rich once you get there.

The Happiness Hedge

It might sound counterintuitive, but one of the best hedges against financial loss is emotional contentment.

During boom times, it’s easy to keep raising the bar – more money, more property, more everything. But if you’re already at a 7 or 8 out of 10 on the happiness scale, chasing a 10 might actually send you backward.

I’ve learned that happiness comes from balance: meaningful work, good health, family time, friends, and enough money to control your schedule. Everything beyond that is gravy over your ego.

So yes, I’m leaning into this AI-driven bull market. But I’m also reminding myself that financial freedom is only worth it if you’re actually free.

Ride the Wave, But Know A Jagged Shore May Await

The energy today feels electric, just like 1999. And I love it. I want to see people make great fortunes so they can have the freedom to do what they want.

Investors could experience an epic blow off like we 26 years ago. Just know how quickly the music can stop. Diversify, stay humble, and take some chips off the table when you can.

Bull markets make you rich. Bear markets make you wise. Together, they make you a complete grizzled veteran.

So let’s enjoy the ride, but with our eyes open!

Question for Experienced Investors:

For those who’ve been investing since 1999 or earlier, how does today’s market feel compared to back then? What similarities and differences stand out to you?

Does the current AI-driven frenzy remind you of the dot-com boom, or does it feel like something entirely new?

Are you positioning yourself for another potential blow-off top that could make us all a lot wealthier or are you bracing for the inevitable hangover?

And for younger investors who didn’t live through 1999, how are you managing your FOMO as everyone around you seems to be getting rich again?

Subscribe To Financial Samurai

Pick up a copy of my USA TODAY national bestseller, Millionaire Milestones: Simple Steps to Seven Figures. I’ve distilled over 30 years of financial experience to help you build more wealth than 94% of the population—and break free sooner.

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Your shares, ratings, and reviews are appreciated.

If you want to stay ahead of the markets, join over 60,000 readers and subscribe to my free Financial Samurai newsletter. You can also get my posts in your e-mail inbox as soon as they come out by signing up here. My goal is simple: help you achieve financial freedom sooner so you can live life on your own terms.

Source: It Feels Like 1999 Again: Time To Party Without Blacking Out